uThukela staff gather outside offices after only some are paid?

The district municipality has managed payment, despite the court order freezing their bank accounts.

uThukela staff are gathered outside the district municipality offices in Lyell Street after some employees were not paid, despite a letter circulating from Municipal Manager Mr LS Jili saying they would all be paid. Some who were paid have not received their medical aid contributions and other allowances. The delay in payments has been blamed on the banks being slow.

Added to the municipal manager’s woes is a letter by DA Councillor Thys Janse van Rensburg, questioning the use of a secondary bank account to pay staff without permission and whether it was legal to circumvent the court ordered freezing of bank accounts.

uThukela payment woes stem from when their bank accounts were effectively frozen.

According to uThukela management, this was because they failed to meet a payment arrangement they had with RASP Consultants CC. From January 21, a court order was obtained, freezing all uThukela bank accounts.

On December 15, uThukela was supposed to honour a court ordered repayment arrangement of R3 million approved by the High Court in October 2025. Despite them failing to make the payment, their creditors initially withheld the full implementation of all possible legal sanctions. What made matters worse is that uThukela had money in their bank account to pay, but did not.

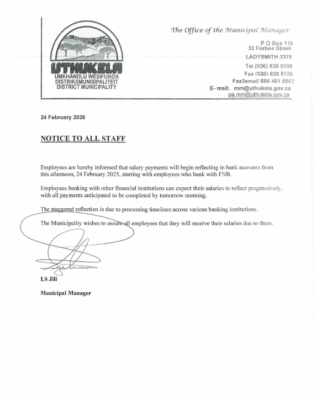

Letter from Municipal Manager

In the letter, Jili assured staff that they would be paid, saying any delays would be due to the banks. A WhatsApp message by Jili was forwarded to staff, saying they had been paid in full, including all allowances due to them, and that they must return to work.

.

Letter to MM

Dear Mr Jili,

Subject: Urgent Inquiry into Reported Use of uThukela Economic Development Agency (UEDA) Bank Account for Municipal Payroll and Related Financial Transactions – Potential Circumvention of High Court Order and MFMA Violations

I write to you in my capacity as a Councillor of uThukela District Municipality, pursuant to Rule 25 of the Standing Rules and Orders (supply of information to councillors) and my oversight responsibilities under the Municipal Finance Management Act (MFMA) No. 56 of 2003. Recent reports indicate that you, as Accounting Officer, have directed municipal funds through the uThukela Economic Development Agency (UEDA) bank account to facilitate partial payment of staff salaries amid the ongoing attachment of municipal accounts by RASP Consultants CC (High Court Case No. 2025-053471).

While the payment of staff is welcomed, the mechanism reportedly used raises serious legal, financial and governance concerns requiring immediate oversight. It is reported that an Economic Development Agency bank account has been utilised in connection with municipal financial transactions.

On available information, there is no known Council resolution authorising:

• the use of a third-party account for municipal payroll purposes; or

• the deposit of municipal-related funds from ILM and Alfred Duma into such an account.

If confirmed, such actions may constitute a deviation from established municipal financial controls and statutory prescripts governing public funds. The use of external accounts for municipal transactions without formal approval presents material risks, including lack of audit trail integrity, weakened financial oversight, and possible exposure to irregular or unauthorised expenditure findings.

This matter arises in the context of the High Court consent order dated 3 October 2025, which you entered into without council approval – a breach of MFMA section 33 (long-term debt commitments requiring council resolution) and section 60 (your fiduciary duties as Accounting Officer).

The order’s clause 7 accelerated the full debt upon default, leading to the attachment on 21 January 2026.

Any redirection of funds through UEDA could be seen as an attempt to circumvent this court order, potentially constituting contempt of court and further violations of MFMA sections 65 (timely payment of debts) and 32 (prevention of unauthorised, irregular, fruitless and wasteful expenditure).

To ensure transparency and compliance, I require a detailed written response within seven (7) calendar days, addressing the following:

1. Origins and Authority for Funds: Provide the exact origins of all funds deposited into and disbursed from the UEDA account for municipal purposes over the past 30 days, including sources (e.g., from ILM, Alfred Duma or other entities), amounts, dates and supporting documentation (e.g., bank statements, transfer records). Confirm whether these funds are municipal in nature and, if so, under what authority (cite specific council resolutions or MFMA provisions) they were redirected.

2. Circumvention of High Court Order: Explain how the use of UEDA’s account complies with the High Court order and attachment writ. Is this not an active attempt to circumvent the court’s directive by routing municipal transactions through a third party entity? Provide legal opinions or advice obtained on this matter, including any risks of contempt or further legal action from RASP.

3. Liability and Accountability: Who authorised these transactions (provide names, positions and dates)? Who bears liability for any irregular, unauthorised or fruitless expenditure arising from this mechanism, including potential personal liability under MFMA section 32(6) or Public Audit Act section 5 (certificate of debt for material irregularities)? Detail steps taken to mitigate risks, such as audit trail preservation and compliance with statutory deductions (SARS, pension funds, medical aid).

4. Governance and Reporting: Why was council not informed of this arrangement in advance, per MFMA section 52(d) (quarterly financial reporting) and Standing Rules Rule 22 (reports to council)? Provide evidence of any prior approvals or risk assessments.

Given the seriousness of these implications, it is recommended that National Treasury and relevant oversight bodies be formally requested to:

– Obtain full statements of the account concerned;

– Review all inflows and outflows;

– Verify payroll disbursement processes; and

– Confirm compliance with statutory deduction obligations (SARS, pension, medical aid,

etc.).

The matter raises significant governance red flags and warrants urgent, independent scrutiny to safeguard municipal funds and ensure compliance with applicable legislation and fiduciary duties.

Failure to respond fully may necessitate escalation to the MEC for COGTA, Provincial Treasury, Auditor-General, and Courts.

I await your comprehensive reply by 4 March 2026.

Yours sincerely,

Thys Daniël Janse van Rensburg (Cllr)