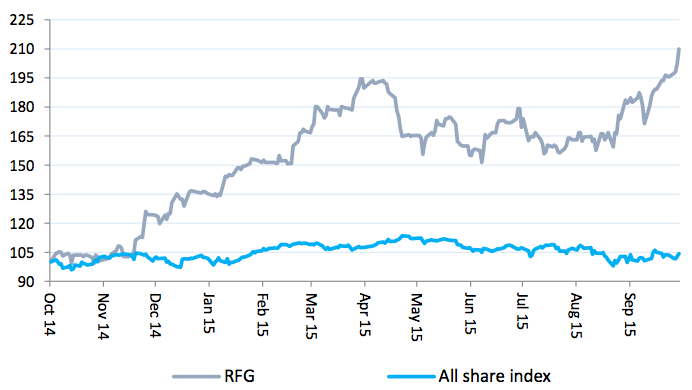

This Western Cape-based food producer is proving to be a noteworthy contender in the food and beverages industry. After some recent corporate actions and clarity on the strategic direction the company is taking we feel its shares are ripe for a buy recommendation.

With products somewhat different from those offered by the likes of Tiger, AVI and Pioneer, Rhodes avoids direct confrontation with its bigger counterparts for most of its products. This gives it a unique advantage of being a dominant niche player with much-needed pricing power for its products. And management‘s acquisition drive spices up the company’s already strong investment case.

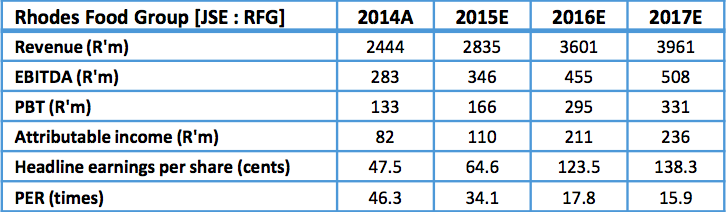

While its valuation, with a price: earnings ratio (PE) of 47, might look a bit intimidating we are not deterred. After unpacking its financials and adjusting for some distortions we arrived at its core PE which is way less than that. Moreover, we think the company’s past earnings history demonstrates that it can command such a high price tag.

The current PE ratio of 47 is calculated based on 12-month basic earnings of 48c/share. According to our largely conservative projections, reported earnings could go up 35% to 65c/share in results for the year to end-September. However, even with such an increase in earnings its PE ratio remains elevated.

The group incurred once-off listing costs of R21.8m or about 10c/share in the interim period. Adding this back to earnings will put projected normalised earnings for the year at 75c/share, resulting in a PE ratio of 30.

But again, we feel this year’s results won’t truly reflect Rhodes’ underlying performance, even after adjusting for the one-off listing costs. Given that three of the four acquisitions made during the year are expected to contribute to operating profit only in the coming financial year, there is potential for an income/costs mismatch.

The company acquired four new businesses for about R330m and much of the purchase consideration is likely to be financed by debt. This will see a significant increase in the interest expense, which will be expensed to this year’s income statement even though there will be little income contribution. For that reason we consider 2016 estimates to be more reflective of its underlying performance than those for the current year.

We project next year’s earnings at 120c/share to 125c/share, giving Rhodes a more reasonable forward PE ratio of around 18.

Rhodes outperformed most of its peers in the food production industry. Its management attributed the strong performance to the strength of its brands, a well-established international customer base and exposure to higher-income groups. The rand’s weakness against Rhodes’ trading basket of currencies also bolstered revenue. Attributable earnings for the interim period to end-March grew 56%, benefiting from lower finance costs flowing through from the lower debt levels, which were slashed after listing in October last year. Net finance costs fell to around 14% of operating income from 45% in the previous year. The operating margin declined to 8% largely because of the R22m listing costs, which were included as part of operating costs.

Revenue growth of 12% was driven by volume growth and price inflation. The rand’s weakness contributed 120 basis points to the growth. Headline earnings climbed 22%. On a normalised basis (excluding listing costs and based on the higher number of shares after listing), headline earnings grew 116% to 36.6c/share (2014: 21.8c)

Having slashed its liabilities just after listing, Rhodes is in a much better position to pursue acquisition opportunities to complement its organic growth strategy. It has a presence in a few African countries, mostly in southern Africa, which leaves scope for growth into potential markets further north.

Management has so far lived up to its listing commitment of accelerating the company’s growth strategy and taking advantage of acquisition opportunities. The four acquisitions provide lateral product extensions and neat entries into the new categories of baby foods, pickles and long-life bottled salads.

Synergistic benefits will flow once the acquired businesses are integrated. Rhodes has an opportunity to cut costs through the centralisation of marketing, production, administration and supply functions of its targets where possible. We think such savings alone could see the company reaching its medium-term goal of an operating margin of 10% (currently around 9%).

The company will also continue benefiting from existing long-term supply partnerships with global and local premium retailers. These provide some assurance over distribution channels. In the past year Rhodes expanded its existing agreement to supply Woolworths with frozen ready meals and dairy products to include pies, pastries and some organic products.

Despite what we see as largely bright prospects, SA’s constrained consumer appears to be the most visible risk to the group’s growth story. This is, however, partly mitigated by Rhodes’ exposure to higher-income customers who are more resistant to the stressed economic environment.

It also has a well-established international customer base from which it generates more than a third of its earnings. While the company hedges some of its foreign currency exposure it will more likely benefit from the weakening of the rand.

Considering that the company could easily more than double its earnings within the next two or three years, Rhodes shares seem like a compelling buy. This view is supported by Intellidex’s discounted cash-flow model which shows 20% upside potential in its shares over the next year. We therefore change our previous recommendation from hold to buy.

Bull factors

• Well-established brand portfolio

• Potential to expand into attractive African markets

• Long-term relationships with premium retailers

• Weaker currency and improved market prices should continue bolstering revenue from international operations

Bear factors

• Consumer spending under pressure

• Competition and price pressures in some of its brands may curb earnings growth

Nature of business: Rhodes Food Group is one of SA’s oldest food producing companies specialising in convenience meal solutions across fresh, frozen and long-life product formats. Its portfolio of brands includes Rhodes, Magpie, Bull Brand, Hazeldene, Portobello and Trout Hall.

Brought to you by Moneyweb