Stellar performance makes it a market darling, but be cognisant of the risks.

On a scale of zero to ten, with below 5 a fail and above 9 exceptional, how significant do you think Naspers’s environmental, social and governance (ESG) concerns are?

This question was put to a panel of asset managers at a RisCura education series on Tuesday, amid growing concern about governance practices at the internet giant.

“I’d say probably a six,” Asanda Notshe, portfolio manager at Mazi Asset Management, said.

“I’d say six or seven. I don’t think it is a significant issue,” Shane Watkins, founder of All Weather Capital, argued.

Co-founder of Sands Capital, Michael Rubin gave the group “five or six”, while Michael Kirsten, founding partner at All Seasons Capital Management, assigned it a “seven [or] eight”.

But Delphine Govender, chief investment officer at value firm Perpetua Investment Managers, was not convinced: “I’d be five. So it’s closer to a fail.”

“Four,” added Anthony Sedgwick, founding member of Abax Investments.

Watkins was taken aback.

“Look, if you are saying it’s a fail and you put it [Naspers] in your portfolio, I think that is inconsistent,” he told Sedgwick, who has been reducing his exposure to Naspers in recent months.

But Sedgwick didn’t budge: If you had a delinquent child, he said, who was extremely gifted in a particular field, but had problems, you didn’t abandon the child, but worked constructively to rectify the behaviour.

“That is exactly what we are doing. I’m not going to give up the greatest potential commercial opportunity for our clients because we have a few [issues]. Every company has its issues… Naspers is no exception,” he said.

The debate highlights the difficult position fund managers and trustees have found themselves in: If they have ignored the counter, it would likely have resulted in underperformance, but its dominant position in various indices means that even a neutral or underweight position could still result in a sizeable exposure to the share (depending on the equity allocation in the portfolio). There are a lot of concerns: What if something went wrong?

Source: RisCura analysis; FTSE/JSE data

Good and bad

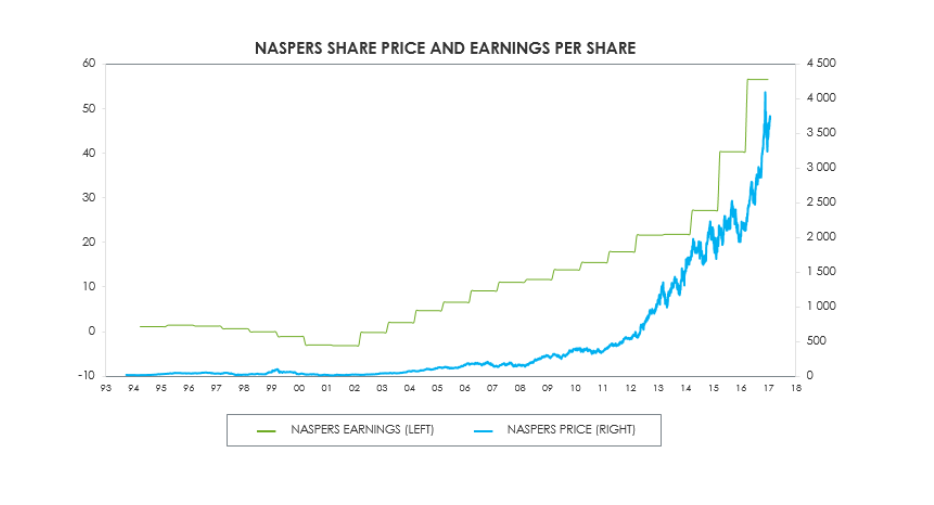

Investors have benefited handsomely from the share’s performance, effectively driven by its 33% stake in Chinese internet conglomerate Tencent. A R100 million investment in Naspers would have grown to R2.3 billion over the past ten years, according to RisCura’s calculations.

Source: Old Mutual Equities

But there has also been widespread criticism against the company’s dual-class share structure – where a small group of shareholders control the vast majority of voting rights – and remuneration policies. There has also been concern about allegations that its subsidiary MultiChoice paid the SABC and ANN7 to influence digital migration policy. Following an internal probe, MultiChoice admitted on Wednesday that it made mistakes, but rejected an assertion that it engaged in corrupt practices.

At the same time, there have also been questions about the variable interest entity structure, which means that foreigners like Naspers investing into Chinese firms like Tencent, do not actually own the shares, but are only entitled to their economic benefit. There is also anxiety about the significant discount at which Naspers is trading relative to Tencent. Effectively, the discount could be seen as the negative value the market assigns to the non-Tencent businesses in the Naspers stable.

Governance

While the issue of governance is often scoffed at, particularly as long as returns are forthcoming, Steinhoff’s recent share price meltdown amidst an accounting scandal has thrust the issue back into the spotlight.

Watkins said under the preamble to Regulation 28 – which governed the allocation of retirement savings to certain asset classes – fund managers had a fiduciary duty to consider any factor that could influence the performance of a share. If fund managers wilfully disregarded ESG factors and there was a subsequent bankruptcy or some other event, they opened themselves up to a case of gross negligence.

The BP oil spill, Marikana massacre at Lonmin and Steinhoff meltdown also highlighted why these factors couldn’t be ignored, he said.

But where does that leave Naspers investors?

Watkins said while there were some ESG issues at Naspers, none of them were so material that it would prevent them from investing in the firm. He engaged quite extensively with Naspers chairperson Koos Bekker about the MultiChoice issue in 2017, even though the engagement didn’t end the way the firm had hoped.

Sedgwick said even though the A and N share structure was a “Jurassic relic” that had to go, the remuneration policy was “wholly unsatisfactory” and the company continued to trade at a significant discount, which had prejudiced minority shareholders, Naspers was a unique asset and had growth prospects that were more exciting than anything else on the JSE in the long term. The share offered currency, geographic and business model diversification and there was value trapped in the corporate structure, which would be unlocked in the long term.

For investors with a five- or ten-year time horizon and the ability to put up with all the issues at the group, it would probably be wise to remain patient, he said.

“But as trustees with big positions in portfolios – you may not have the extent of that luxury. Our view – certainly in our client portfolios – is no matter how much we like it we are not going to have 25% of our client portfolios in a single stock, regardless of how diversified it is.”

A SWIX weight of around 25% was inappropriate, he added.

But Govender was not convinced.

“We don’t own Naspers in our portfolios because we are concerned about the opacity of this group structure. We are concerned about management’s capital allocation. What had been historically very good has started to deteriorate in our opinion… We believe that the rate of growth of Tencent is going to taper from current levels. We look to invest in shares that offer value and we think that the market is choosing to selectively avoid emphasising some of the risks.”

Brought to you by Moneyweb

Support Local Journalism

Add The Citizen as a Preferred Source on Google and follow us on Google News to see more of our trusted reporting in Google News and Top Stories.