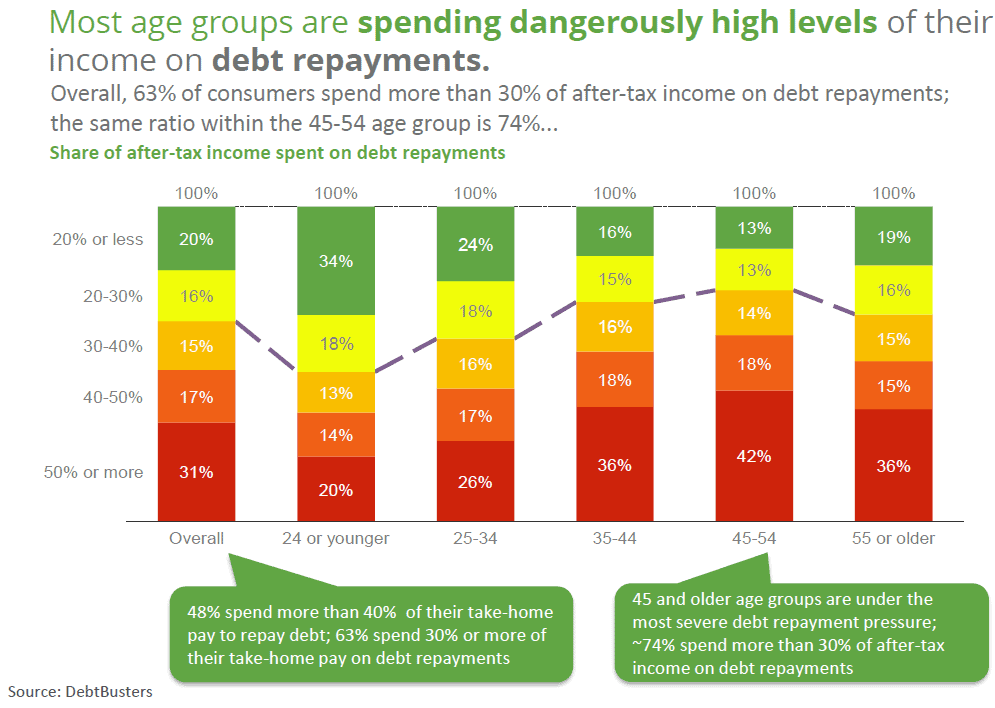

Overall, 63% of consumers spend more than 30% of after-tax income on debt repayments; the same ratio within the 45-54 age group is 74%.

Picture: iStock

Although South Africans are experiencing notably less financial stress than they did for the past two years, with levels of financial stress returning to levels last experienced in 2022, money stress remains a significant issue for many people.

According to the fourth annual DebtBusters Money-Stress Tracker which surveyed more than 27 000 respondents during May and June:

- 70% of respondents experienced money stress, down from 78% in 2023 and 75% in 2024. Although the extent of financial anxiety is declining, the impact on daily life remains substantial. Among respondents who said they still experience financial stress, 91% of them felt it affected their home life, 73% their work life and 73% their health.

- Women still bear a disproportionately higher burden of financial stress, with almost three out of four female respondents reporting feeling financially stressed. Women are around 10% more stressed about finances and 20% more stressed about work life, home life and health compared to men, although stress levels for both genders decreased by 5% to 15% across all facets of life since 2024. The shift is attributed to fewer national crises, such as less load shedding, reduced inflation and people starting to manage their finances better, allowing them to look beyond short-term survival.

ALSO READ: Survey shows how economic distress erodes South Africans’ savings culture

Even small improvements decrease financial stress

The Money-Stress Tracker worked with psychologist Andrea Kellerman, who notes that even a 5% drop in financial stress (from 75% to 70% in the past year) results in people sleeping and coping “a bit better,” suggesting the profound impact even small improvements can have on resilience and perception.

However, there are still key financial concerns. For people battling with financial stress, short-term concerns continue to dominate, with the top two running out of money before the end of the month and struggling to pay off monthly debt.

The impact of interest rate increases, while still significant, subsided compared to 2023 and 2024.

ALSO READ: Sarb: financial stability but financial distress in households and SMEs

Different age groups have different levels of financial stress

The survey shows that people from different groups have more or less financial stress:

- Age: Middle-aged (35 – 44 years) respondents had the most financial stress. Concerns about retirement increased for respondents older than 45 compared to 2024, indicating that this age group can now look beyond the short-term concerns which traditionally dominate.

- Income: Lower-income groups are the most concerned about the impact of interest rate increases or unexpected expenses. While electricity costs are an elevated concern across all income groups compared to 2024, retirement worries are more pronounced in the upper-income brackets. People earning more than R20 000 a month remain in the group that experiences the most financial stress, often qualifying for and taking on more credit than their earning capacity allows.

- Region: Respondents from the Western Cape are the most financially concerned, surpassing Gauteng, which reported the most financial stress in 2024. The Western Cape is also where most people worry about unexpected expenses and retirement. Smaller provinces, such as the Northern Cape, Limpopo and Mpumalanga, saw significant increases in concerns about electricity costs and interest rates.

The survey also investigated borrowing and debt repayment trends and found:

- 63% of respondents allocated 30% or more of their after-tax income to debt repayment, while 48% spend over 40% paying back what they borrowed, a level considered unsustainable.

- People older than 45 are under the most severe debt-repayment pressure, with 60% having unsustainable levels of debt.

- Respondents earning more than R20 000 a month also face considerable pressure to repay debt.

This chart shows how much of their income the respondents spent on repaying debt:

ALSO READ: How to minimise financial stress in your life

What people are doing to combat financial stress

However, the survey also shows that they are actively doing something about their financial stress:

- 37% of respondents reported actively cutting back on monthly spending, compared to 43% in 2022. This suggests savings fatigue has set in, Kellerman says.

- Seeking higher-paying or better jobs is a growing trend, with 35% of consumers exploring these options to make ends meet, compared to 26% in 2022.

- Younger consumers are more proactive about sticking to budgets and are almost four times more likely to seek better employment. The survey shows that 56% of the respondents are more intent on managing financial stress than people older than 35.

- Respondents elaborating on how they manage financial stress revealed a shift in coping mechanisms. In 2022 and 2023, people tended to seek better jobs or start a side hustle, while in 2024, debt counselling was the preferred way to relieve financial stress. Now there is a growing emphasis on entrepreneurial efforts, multiple income streams and financial independence, reflecting a move towards self-reliance and creating diverse sources of income.

Benay Sager, executive head of DebtBusters, says that despite the slight reduction in overall stress, over 90% of South Africans with unsustainable debt do not proactively seek professional support such as debt counselling.

“This underscores the ongoing importance of stress-management programmes, financial education and awareness campaigns that address stigma and promote early intervention. It also highlights the need for innovative solutions to deal with financial stress, particularly those that help consumers stretch their money further.”

ALSO READ: South Africans remarkably resilient despite economic challenges

With less financial stress, people are sleeping and coping better

Kellerman says the 2025 edition of the Money-Stress Tracker brought an encouraging insight that some might overlook at first glance: while overall financial stress levels dropped from 75% in 2024 to 70% in 2025, the impact of this change could be substantial.

“People are sleeping and coping a bit better despite elevated financial pressure. This “disconnect” between the data and lived experience tells an important story about resilience, perception and the compounding effects of small improvements.

“It is well known that perception drives behaviour, and in 2025, that is more evident than ever. Although financial stress and pressure remain high for many, people report feeling more in control, more optimistic, as well as more willing to engage with support structures.

“However, for the first time in years, there was an overall sense of stability. The absence of large-scale disruptions such as load shedding or social unrest allowed people to regain emotional bandwidth and reframe their financial situation. With just a small decline in stress, people have begun to look beyond short-term survival.”