Lower borrowing costs open doors for home buyers

Falling interest rates, rising approval rates and lower deposits are opening doors for South African homebuyers, especially first-time buyers, amid improved affordability.

The latest home loans data, released by ooba Home Loans, South Africa’s foremost home loan comparison service, points to improvements across all major indicators, set against the backdrop of a lower interest rate environment.

“Our Quarter 2 2025 (Q2 ’25) oobarometer highlights an upturn in home loan activity, primarily driven by improved affordability – where income growth outpaces house price inflation in some regions – and the reduced cost of borrowing,” says Rhys Dyer, CEO of the ooba Group.

He adds that in addition to the 1% year-on-year reduction in the cost of borrowing, the banks remain highly competitive, offering some of the largest discounts to the prime lending rate seen in recent years.

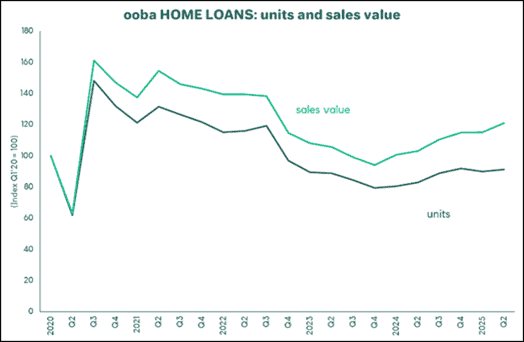

“These culminating factors have yielded positive outcomes, with ooba Home Loans’ application volumes rising by 11% year-on-year and the total value of these applications increasing by 18.5%,” continues Dyer. “These figures signal a decisive rebound from the post-pandemic slump that bottomed out in Q4 ‘23.”

Source: ooba Home Loans

Improved affordability spurs higher home buyer spending

Q2 ‘25 data shows that homebuyers (now one-year older year-on-year – aged 40) are spending more, with the average property purchase price increasing by 3.9% year-on-year – now at R1,695,257.

Regionally, Dyer highlights substantial increases in average purchase prices, especially in the Free State and Tshwane. “From January to June ‘25 (H1 ‘25), the Free State and Tshwane saw significant year-on-year growth in the average purchase price paid – up by 12% (R1.16 million) and 10.1% (R1.77 million), respectively. Tshwane also registered the highest growth in average monthly gross income for the same period, up by 15.9% to R78,713 – highlighting improved affordability as a key driver in the region’s improved performance.”

Meanwhile, the country’s most expensive region, the Western Cape, recorded a modest 3.3% year-on-year increase in the average purchase price, bringing it up to an average of R2.39 million while Johannesburg’s purchase price rose by 5% to R1.65 million (H1 ‘25).

“With the exception of Gauteng South & East, every region recorded an increase in the average purchase price over the quarter from year-earlier levels – a promising indicator for the market at large.”

Bank lending ramps up

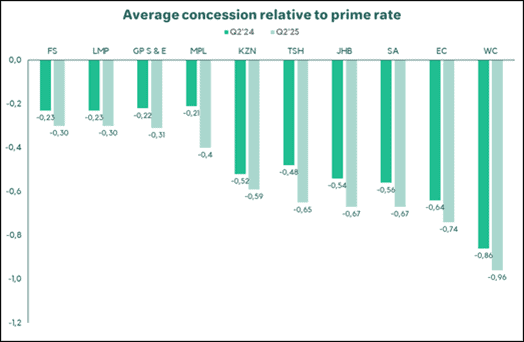

In Q2 ‘25, ooba Home Loans achieved an average interest rate of prime less -0.67% for its customers – a notable improvement of -0.11% on Q2 ‘24 and -0.12% on Q1 ‘25.

While all regions enjoyed attractive interest rate discounts in Q2 ‘25, the Western Cape achieved the highest average discount, at prime less -0.96%, followed by the Eastern Cape at -0.74%. Year-on-year, Mpumalanga and Tshwane saw the biggest improvements in their pricing, with rate discounts up by -0.19% and -0.17%, respectively.

Source: ooba Home LoansAdding to robust bank lending activity, approval rates for ooba Home Loans’ customers remained elevated in Q2 ’25 at 82.6% – flat on Q2 ‘24, while the ratio of applications declined by one bank but approved by another increased to 45.7%, highlighting the importance of shopping around to multiple banks for a home loan.

Deposits drift lower

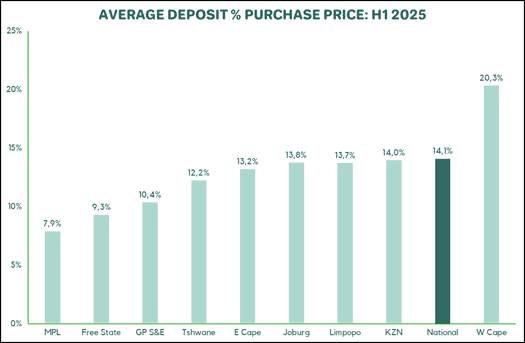

Home loan deposits drifted lower in Q2 ‘25 relative to the same period last year, down by 13.5% year-on-year to R239,545. Despite the drop, deposits still represent a substantial 14.1% of the average purchase price.

Regionally, Dyer shares that the Western Cape recorded the highest average deposit for the quarter, at 20.3% of the purchase price, while Mpumalanga came in lowest at 7.9%. “Tshwane, the Eastern Cape, Johannesburg, Limpopo, and KwaZulu-Natal posted deposit values ranging from 12.2% to 14.0% of the purchase price – reflecting strong saving habits and a clear understanding of the importance of putting down a deposit on a home loan,” he adds.

New horizons for South Africa’s first-time home buyers

First-time homebuyers (aged 35 on average in Q2 ‘25, unchanged from year-earlier levels) are responding positively to the current home loan environment, spending 3.5% more on homes in Q2 ‘25 than in Q2 ‘24 (at R1,239,413).

And although the percentage of first time homebuyers showed only a modest year-on-year (increase of 1%) to 46% in Q2 ‘25, Dyer expects demand from this segment to gradually rise following July’s expected interest rate cut.

“Banks are actively stimulating this market segment by offering attractive incentives, such as zero-deposit and cost-inclusive home loans,” he notes.

59% of first-time homebuyers purchased without a deposit (100% home loans) and 10.5% secured financing that also covered transfer and bond registration costs. He adds that the overall approval rate in this segment for home loans with a loan-to-value (LTV) ratio of 100% or more still reflects a very strong 80.8% in Q2 ’25 – slightly lower than the 81.7% recorded in Q2 ‘24.

Buy-to-let activity maintains momentum

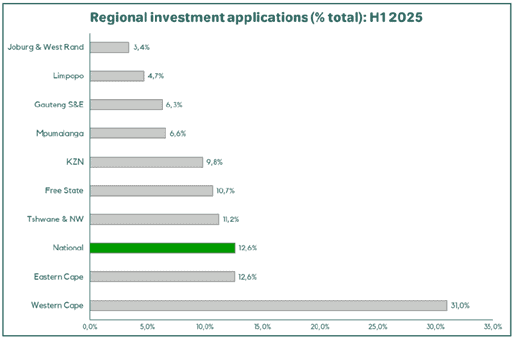

National demand for buy-to-let properties remains steady, accounting for 12.6% of total applications for H1 ‘25 – a slight increase from 12.2% over the same period in 2024.

“The Western Cape continues to garner strong interest, with demand holding steady at around 31% of total applications, ” says Dyer. And while investment demand in the Eastern Cape eased to 12.2%, down from a peak of 20% in December ‘24, the region maintains a solid share of the market.

Looking ahead, Dyer believes there is a strong likelihood of another interest rate cut in July – a development that will play a key role in driving a successful second half of the year. “More South Africans can step into the property market with confidence, knowing that all key indicators are gaining ground and that the banks are willing to support them. We anticipate stronger demand from first-time homebuyers, in particular, over this period and look forward to supporting them on their journey to homeownership.”

Issued by: Jess Gois