Some sectors are better off than others, but the impact on individuals will be felt in various ways.

Archive photo: Ashraf Hendricks, GroundUp

The Covid-19 pandemic and subsequent economic and social lockdowns have had a negative impact on the world economy, the extent of which has not been seen since the Great Depression.

The global economy is expected to decline by 3% in 2020 according to the International Monetary Fund (IMF). Advanced economies are likely to be hardest hit and are expected to contract by 6.1% according to the IMF.

Conversely, it is anticipated that emerging markets will decline by 1%. In Finance Minister Tito Mboweni’s June 24 supplementary budget speech he painted a gloomy picture of a struggling economy that will be tested to its limit to maintain fiscal stability.

Among the more concerning statistics:

- The budget deficit for 2020 is expected to be 15.7%, increasing from a forecast of 6.8% in the February 2020 budget speech;

- This large budget deficit will result in the deterioration of SA’s debt-to-GDP ratio from 63.5% to 81.8%;

- South Africa’s economy is expected to contract 7.2%; and

- A R300 billion revenue collection shortfall is expected.

These figures are purely financial and relate to the gap between revenue collection and expenditure.

Statistics SA recently released the unemployment rate for the first quarter of 2020 according to the quarterly labour force survey. This figure has breached the 30% barrier and is recorded as 30.1%.

The largest cause for concern is that the first quarter was only affected by the lockdown for a few days. The rate is expected to rise when the unemployment statistics for the second quarter are released.

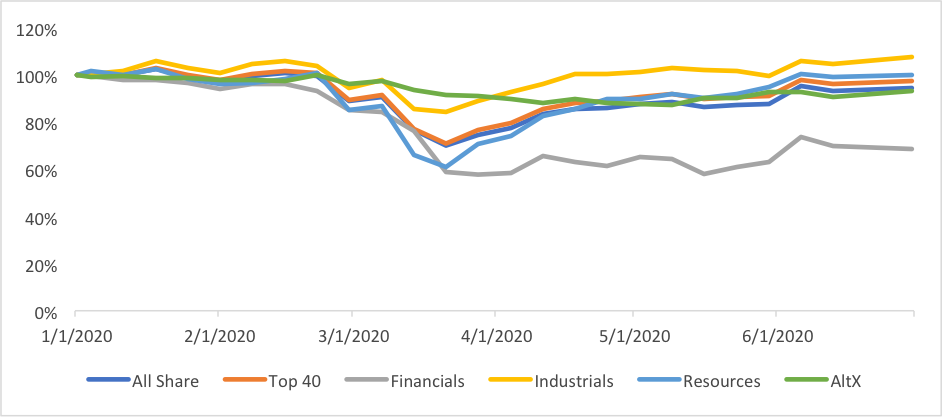

The effects of the impact on the global and local economy have been felt on stock markets across the world and the JSE is no different. The graph below illustrates how the aggregate indices on the JSE performed in the first six months of 2020.

JSE index performance – January to June 2020

Source: 21st Century

The graph illustrates that, universally, all industries felt the negative impact of the Level 5 Lockdown period in March and April. The AltX experienced the shallowest decline over this period, but has not returned to the levels it was at at the end of 2019.

Conversely, the deepest contraction on the JSE has been within the financial sector, which has not recovered from the decline it experienced in March and April.

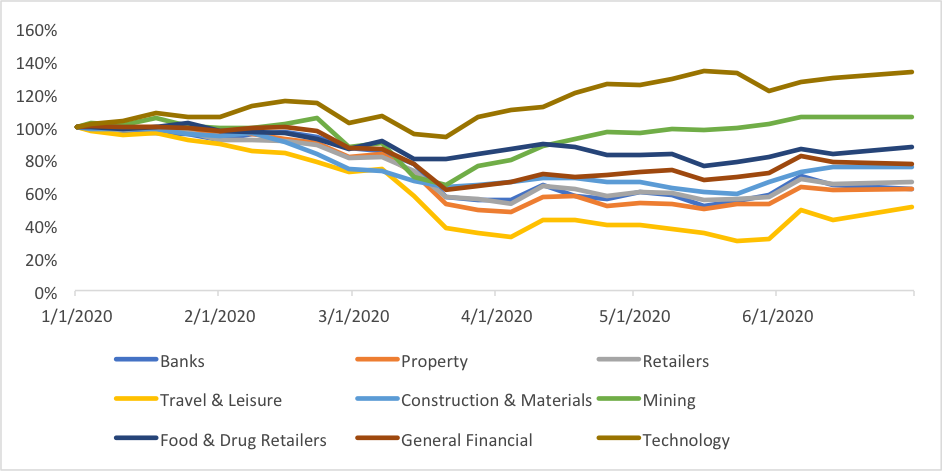

Analysing the JSE sectors at a deeper level indicates that there have been winners and losers over this period, albeit that there have been more losers. The following graph illustrates how the various JSE sectors have performed over the first six months of 2020.

JSE sector performance – January to June 2020

Source: 21st Century

The graph indicates that banks, property, retailers and the travel and leisure industries have suffered the deepest decline in their share prices.

Conversely, mining and technology are the only two sectors that have experienced an increase (year to date) in their aggregate share price.

These share price indicators provide a yardstick to measure how well each sector is performing, and this is directly linked to how employees have been affected within these industries.

According to Stats SA, formal employment declined within all reported sectors other than mining, trade and private households. The expectation is that this negative employment outlook will deteriorate in the second quarter as the true effect of the lockdown is tabled.

The theme of negative performance on the stock exchange has further reaching consequences for employees beyond the initial employment concerns. The negative impact has also resulted in numerous companies having to implement salary reductions as a means of cost cutting over this period.

Pension funds and other financial instruments are presently navigating an economic minefield as they seek to guard against or limit losses in the present environment.

Impact on incentive schemes

Share-based long-term incentive schemes will also be affected by the negative performance on the JSE. Typically, long-term incentive share schemes either offer full shares (holder receives full value of shares) or appreciation shares (holder only benefits from the difference between the value of the share and price at which it was issued).

Full shares still hold benefit for the holder as long as the share exists as the cost of the share was zero. Conversely, the economic headwinds experienced in 2020 so far have put pressure on many appreciation share schemes as a result of factors outside of the control of the company (the effects of Covid-19 on the economy).

This has put many of these share schemes ‘underwater’ (they do not have a positive yield for the holder).

The data from the JSE suggests that apart from mining and technology, other industries’ share price indices are below the levels that they were at on January 1.

The other sectors of the JSE may have individual winners, but the sectoral view is that their indices are below where they were at the start of the year. This negative impact on companies has cascaded from corporate level to employee level as jobs have been lost and salaries have been reduced as a means of ensuring the survival of the company.

Given the reliance of South Africans on their monthly income and SA’s historically poor household savings, the loss of jobs and reductions of incomes have been particularly painful for SA citizens.

There have been very few economic winners in 2020 and unfortunately the long list of economic losers looks set to grow as we await the economic data from the second quarter, which will include the full lockdown period.

This article first appeared on Moneyweb and was republished with permission.

For more news your way, download The Citizen’s app for iOS and Android.