The Middle East and Africa (MEA) smartphone market has stumbled into 2026.

Smartphones. Picture: iStock

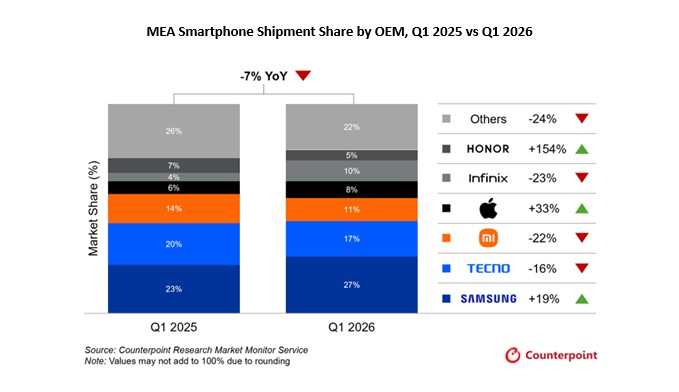

The Middle East and Africa (MEA) smartphone market has stumbled into 2026, posting a 7% year‑on‑year decline in Q1 shipments, according to Counterpoint’s latest Market Monitor.

After several quarters of growth, the downturn marks the region’s first contraction since 2025, driven by surging handset prices, limited availability of entry‑tier models, and escalating regional conflicts that have disrupted supply chains and consumer demand.

Entry tier

The entry‑tier segment, long the backbone of MEA volumes, bore the brunt of the decline, with shipments in the $50-$99 band plunging 41% year-on-year (YoY).

Rising memory costs and geopolitical instability have compounded the squeeze, leaving shelves empty in several markets and pushing consumers to delay upgrades.

Analysts warn that Q2 2026 could see further declines, with few sales‑driving occasions on the horizon and intensifying macroeconomic headwinds.

5G smartphones

Despite the overall slump, premiumization trends remain visible. 5G smartphone shipments surged 42% YoY, buoyed by expanding coverage and the planned sunset of 2G and 3G networks.

AI‑capable devices also grew 64% YoY, though adoption remains concentrated in the $400‑plus price tier, underscoring the widening gap between premium and mass‑market consumers.

Brands

Brand performance diverged sharply. Samsung strengthened its regional dominance with 19% YoY growth, supported by stable pricing, robust inventories, and the launch of its flagship S26 lineup.

Honor delivered a remarkable 154% surge, leveraging a low base, steady stock, and strong positioning in GCC premium markets. In contrast, Chinese OEMs such as Transsion and Xiaomi struggled with supply shortages, leaving retail shelves bare in parts of the Middle East, though Africa remains a key stronghold for Tecno and itel.

Pressure

Macro pressures are adding to the strain. Rising layoffs and corporate downsizing in GCC economies are eroding purchasing power, while spikes in fuel and logistics costs are inflating consumer goods prices.

With uncertainty reshaping buying behaviour, purchases are increasingly driven by necessity rather than upgrades or premium aspirations.

As the MEA market braces for Q2, the outlook remains fragile. Without relief from memory pricing and geopolitical instability, the region’s smartphone industry faces a challenging year ahead, with premium players better positioned to weather the storm than entry‑tier brands.